What if the "magic number" you've been told you need for retirement is actually the least important part of your financial plan? Most Australians spend years fixated on a single lump sum, yet they still feel a persistent anxiety when they think about actually resigning. You likely understand this tension; the fear that a sudden market dip or a complex change to Superannuation rules could compromise your lifestyle before you've even started to enjoy it.

It's a valid concern. However, sophisticated retirement cash flow modeling replaces this uncertainty with a structured, evidence-based roadmap that accounts for the 12.0% Superannuation Guarantee and the latest tax thresholds. In this article, you'll discover how to transform dense financial data into a visual "green light" for your future. We'll explore how to optimise your Super and Centrelink benefits together, ensuring you have the clarity to stop working with absolute confidence.

Key Takeaways

- Transition from the anxiety of accumulation to a structured decumulation strategy that prioritises longevity and lifestyle stability.

- Understand how sophisticated retirement cash flow modelling stress-tests your wealth against market volatility and sequence of returns risk.

- Navigate the complexities of the Transfer Balance Cap and Centrelink rules to ensure your retirement income is both tax-efficient and sustainable.

- Learn how to categorise your future expenses into needs, wants, and wishes to create a bespoke roadmap that reflects your personal goals.

- Discover how a research-driven approach to portfolio construction provides the clarity you need to stop working with absolute confidence.

What is Retirement Cash Flow Modelling?

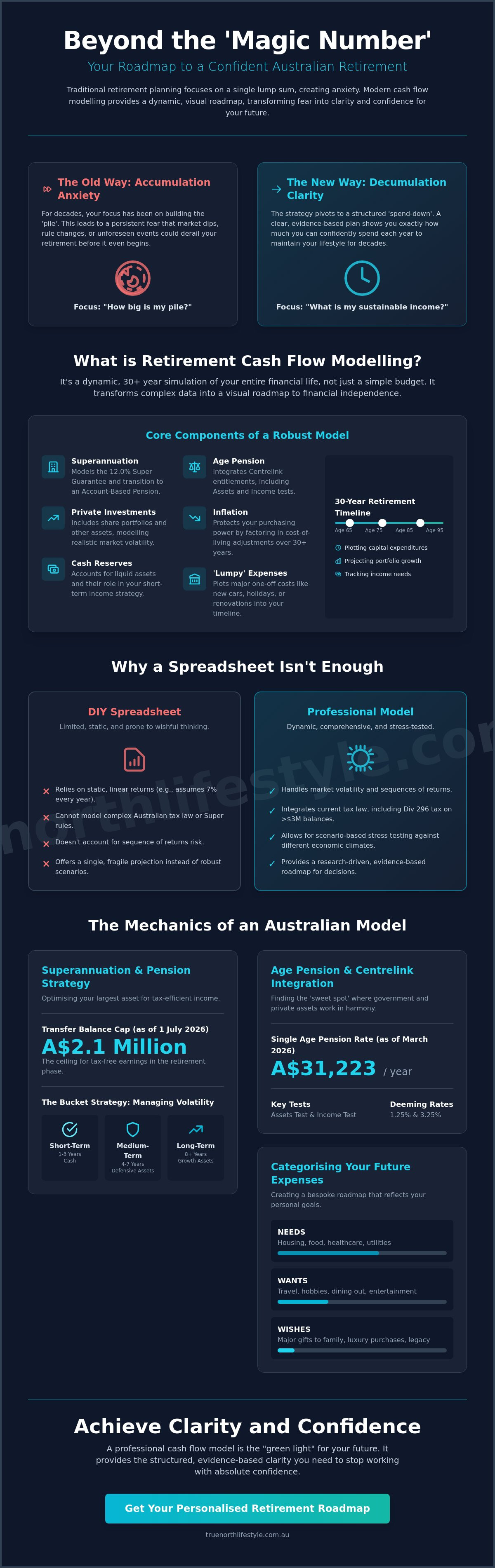

Clarity replaces fear. Retirement cash flow modeling is not a simple calculation; it is a dynamic, longitudinal simulation of your financial existence. While a budget tracks what you spent last month, this model projects what you can safely spend over the next thirty years. It serves as a comprehensive visual roadmap, transforming abstract numbers into a tangible plan for your future.

For most of your working life, the focus was on accumulation. You were building the "pile." As you approach the end of your career, the strategy must pivot toward decumulation, or the retirement spend-down process. This shift is often the source of significant anxiety. The model provides the evidence needed to move from a mindset of scarcity to one of confident spending. It identifies the exact moment you achieve true Financial Independence; the point where your assets can sustain your lifestyle without the need for further employment income.

The Core Components of a Robust Model

A sophisticated retirement cash flow modeling exercise is far more than a single account projection. It integrates every facet of your financial world, including Superannuation, private share portfolios, and cash reserves. It also factors in the safety net of the Age Pension, which provides A$31,223 per year for singles as of March 2026. This isn't a static snapshot. It is a living strategy that accounts for the 12.0% Superannuation Guarantee and cost-of-living adjustments.

Longevity requires accounting for the silent thief of inflation. Over a thirty-year retirement, the purchasing power of a dollar can diminish significantly. A robust model also anticipates "lumpy" capital expenditure. Whether it's a A$70,000 kitchen renovation or a new vehicle every eight years, these expenses are plotted into the timeline to ensure they don't derail your long-term sustainability.

Why a Spreadsheet Isn’t Enough

DIY Excel sheets are inherently limited. They often rely on static, linear returns, assuming your portfolio grows by exactly 7% every single year. In reality, markets fluctuate. Professional software handles these complexities, including the intricate web of Australian tax law and the new Division 296 tax on balances exceeding A$3 million. For small business owners, integrating these variables with advice from The Bucket List Accountant allows for scenario-based thinking rather than just wishful guessing.

True North Lifestyle acts as the Steady Navigator in this process. We use research-driven data to stress-test your strategy against different economic climates. This disciplined approach moves you away from the "hope and pray" method of retirement planning. Instead, it places you in a position of confident oversight, where every decision is backed by rigorous testing and logical structure.

The Mechanics of an Australian Retirement Model

Structure creates stability. A professional retirement cash flow modeling exercise isn't just a series of graphs; it's a complex engine that processes the interlocking gears of Australian regulation. It moves beyond the "pile of money" mindset and focuses on how that wealth is distributed, taxed, and preserved over decades. By simulating the interaction between different asset classes and regulatory caps, we can identify potential shortfalls long before they become crises.

Superannuation and Pension Account Projections

The transition from the accumulation phase to an Account-Based Pension is a pivotal moment. This shift requires a deep understanding of the Transfer Balance Cap, which serves as a critical ceiling for tax-free earnings within the retirement phase. As of 1 July 2026, this cap is A$2.1 million. A robust model must also account for mandatory minimum withdrawal rates, which increase as you age, ensuring your strategy remains compliant while providing the necessary liquidity for your lifestyle.

Tax-minimisation remains a priority even after you stop working. We utilise the "Bucket Strategy" to segment your wealth into short-term cash, medium-term defensive assets, and long-term growth investments. This visual component of the model ensures you aren't forced to sell growth assets during a market downturn, providing a sense of order and protection against volatility.

Factoring in the Age Pension and Centrelink Structuring

Clarity on government entitlements is essential for a sustainable roadmap. Modelling helps identify the "sweet spot" where your private assets and the Age Pension work in harmony. We examine the interaction between the Assets Test and the Income Test, particularly as deeming rates sit at 1.25% and 3.25% as of March 2026. Even for self-funded retirees, understanding how "Gifting Rules" impact long-term projections is vital for estate planning and wealth preservation.

Sydney families, especially those in the Sutherland Shire, often find that generic national standards don't reflect their reality. While the ASFA "comfortable" standard for a couple is A$74,423 per year, maintaining a premium lifestyle in NSW typically requires a more nuanced approach. While some may look to generic retirement planning tools for basic guidance, these lack the local precision required for high-net-worth individuals. Achieving this level of detail requires a bespoke portfolio construction that accounts for your specific "Needs, Wants, and Wishes" in a local context.

Stress-Testing the Strategy: Static vs. Dynamic Modelling

Confidence requires testing. The most frequent concern we hear from Sydney families is the fear of a market crash occurring exactly when they stop working. This isn't just pessimism; it's a recognition of "Sequence of Returns Risk." If the market dips significantly in the first few years of your retirement while you're also withdrawing capital, the long-term sustainability of your portfolio can be compromised. Professional retirement cash flow modeling addresses this head-on by moving beyond static, linear projections.

We don't rely on historical averages alone. Instead, we utilise Monte Carlo simulations to stress-test your strategy against 1,000 or more potential market scenarios. This process identifies the probability of your capital lasting until age 100, rather than just 85. By simulating various economic climates, including GFC-style events, we can determine if your roadmap is truly resilient. This rigorous approach to Planning for Cash Flows in Retirement ensures that your "Plan B" is already built into the foundation of your strategy.

The Impact of Market Volatility

Order replaces chaos. A robust stress test allows you to see how your specific assets would behave during a prolonged downturn. It's about worst-case survival, not just best-case growth. Knowing that your "Bucket Strategy" provides enough cash and defensive reserves to weather a three-year market slump offers a profound emotional benefit. You'll find the certainty to stay the course when others are panicking, as your retirement cash flow modeling has already accounted for these fluctuations.

Longevity and Healthcare: Planning for the Long Tail

Longevity is a risk that requires disciplined oversight. With Australian life expectancy now exceeding 85 years, your savings may need to provide for three decades or more. We must also account for the rising cost of healthcare, which is currently increasing at approximately 7% annually. A comprehensive model factors in these escalating costs in your final decade, ensuring you aren't left vulnerable when you need support the most.

Your home often serves as a final cash flow pillar. We can model "downsizing" scenarios where home equity is released to bolster your liquid assets or fund aged care requirements. This isn't about selling the family home out of necessity; it's about strategic construction. By integrating these scenarios into your bespoke portfolio construction, we ensure your wealth preservation strategy remains as dynamic as the life you choose to lead.

Step-by-Step: Preparing for Your Professional Modelling Session

Preparation is the bridge between anxiety and order. To build a robust simulation, we require the raw materials of your financial life. This data collection phase involves gathering current Superannuation statements, bank balances, and a clear picture of any outstanding liabilities. While these numbers provide the foundation, the true value of retirement cash flow modeling emerges during the "Lifestyle Discovery" phase. Here, we move beyond the ledger to define your Needs, Wants, and Wishes.

This is an iterative journey. We explore different scenarios; perhaps retiring at 62 instead of the intended age pension age of 67, or evaluating the impact of a significant downsizing event. As your Authoritative Guide, we navigate these variables to find the path that offers the greatest stability. We move the conversation from "can I afford this?" to "this is how we make this happen." This process ensures that the transition from work to leisure is not a leap of faith, but a calculated step into a well-defined future.

Defining Your Retirement Income Goal

Clarity begins with a pay cheque. We distinguish between "Essential" cash flow; the non-negotiables like insurance, utilities, and groceries; and "Discretionary" spending. For Sydney residents, estimating these costs requires precision. While the ASFA "comfortable" standard provides a baseline of A$74,423 for a couple as of June 2025, many of our clients find their actual "Wants" category requires a more tailored approach. This might include international travel, high-end hobbies, or strategic gifting to grandchildren. Honesty in this phase is paramount. It ensures the model reflects the life you actually intend to lead, not a compromised version of it.

The Review and Refinement Process

A roadmap is only useful if it reflects the current terrain. Because markets and regulations shift, your model must be updated annually to incorporate real-world returns and legislative changes like the 12.0% Superannuation Guarantee. This ongoing review allows for tactical decisions, such as adjusting drawdowns during high-inflation periods to preserve capital longevity. Once the modelling is finalised and stress-tested against the sequence of returns risks discussed previously, the insights are formalised into a comprehensive retirement modelling and long-term projection strategy. This transition from a visual model to a formal Statement of Advice (SOA) provides the legal and strategic framework to move forward with quiet certainty. This structured progression ensures that your financial future is not left to chance, but is instead the result of disciplined, research-driven construction.

Achieving Clarity with True North Lifestyle

Order replaces anxiety. At True North Lifestyle, we act as the Steady Navigator for Sydney families who seek to move beyond the "hope and pray" method of financial planning. Our approach to retirement cash flow modeling is not merely a technical exercise; it's a commitment to your long-term emotional reassurance. We understand that behind every spreadsheet lies a human story of hard work, sacrifice, and the desire for a protected future.

Our methodology is fundamentally research-driven. We don't rely on market sentiment or flashy trends. Instead, we focus on bespoke portfolio construction that prioritises wealth preservation and low-volatility outcomes. Through our collaboration with Resonant Asset Management, we apply rigorous testing to ensure your capital is managed with the highest level of discipline. This partnership allows us to build strategies designed to weather market fluctuations while providing a steady, reliable income stream for decades to come.

We welcome you to visit our offices in Miranda or the Sydney CBD for a personal projection. These sessions are designed to provide a high-level view of your potential trajectory, allowing you to step into a role of confident oversight. We've already done the heavy lifting and the rigorous testing; your role is to provide the vision for the life you wish to lead. Whether you're navigating the new Division 296 tax rules or simply want to know when you can stop working, we provide the logical grounding you need.

The True North Difference: Professionalism and Empathy

Complexity often leads to paralysis. Our "Simplifying the Complex" philosophy, particularly at our Miranda office, is designed to strip away the jargon and focus on what truly matters. We remove the anxiety of the unknown by providing a structured, evidence-based roadmap that you can actually understand. This isn't just about numbers on a page. It's about the quiet certainty that comes from knowing your wealth preservation strategy is built on a foundation of logic and proven outcomes. We provide the stability you need to make informed choices without feeling overwhelmed by the shifting landscape of Superannuation and tax law.

Your Next Steps Toward Retirement Confidence

Clarity is within reach. We invite you to a no-obligation consultation to begin the modelling process and discover the "green light" for your retirement plans. This initial conversation is the first step toward achieving the stability and longevity you've worked so hard to secure. The outcome is more than just a financial plan; it's the freedom to enjoy your future without the weight of persistent uncertainty. You deserve a partner who values trust and proven results over flashy innovation. Secure your financial future with a bespoke retirement model and begin your journey toward a calm, ordered retirement today.

Step into Your Future with Quiet Certainty

True financial independence is more than a number in a bank account. It's the result of a disciplined process that replaces the anxiety of the unknown with a structured, evidence-based roadmap. By utilising sophisticated retirement cash flow modeling, you move beyond guesswork and into a position of confident oversight. You've seen how stress-testing your strategy against sequence of returns risk and integrating complex Superannuation rules provides the clarity needed to stop working on your own terms.

True North Lifestyle acts as your Steady Navigator. As specialists in Sutherland Shire retirement strategies, we provide stabilising advice that focuses on the human outcome of your financial decisions. With research-driven Investment Committee oversight and a commitment to bespoke portfolio construction, we ensure your plan is as resilient as it is personal. It's time to replace uncertainty with order.

Book a Retirement Modelling Consultation with our Sydney Experts and begin building your roadmap today. You deserve the peace of mind that comes from a well-defined path.

Frequently Asked Questions

How much does professional retirement cash flow modelling cost in Australia?

Professional fees for strategy construction typically reflect the complexity of your financial situation. Most reputable firms charge a flat, transparent fee for the initial modelling and Statement of Advice rather than a percentage of your assets. This structure ensures that the advice remains objective and focused entirely on the construction of your long-term roadmap. You should view this as an investment in the clarity and order of your future.

Can modelling help me get more Age Pension from Centrelink?

Yes, sophisticated modelling identifies the most efficient ways to structure your assets for Centrelink purposes. By simulating the interaction between the Assets Test and the Income Test, we can often uncover opportunities to optimise your Age Pension eligibility. This is particularly vital given that deeming rates sit at 1.25% and 3.25% as of March 2026. Small structural changes can lead to significant improvements in your total retirement income.

How often should I update my retirement cash flow model?

You should review and update your model at least once every year. Regular updates allow us to incorporate real-world investment returns and adjust for legislative shifts, such as the Superannuation Guarantee reaching 12.0% in July 2026. You also need to refresh the model immediately following major life events. An inheritance, a property sale, or a significant change in health requires a tactical recalibration of your strategy to maintain its longevity.

Is retirement modelling accurate if the stock market is volatile?

Accuracy in retirement cash flow modeling is not about predicting market movements, but about preparing for them. We use Monte Carlo simulations to stress-test your portfolio against 1,000 different market scenarios, including prolonged downturns. This process ensures that your strategy is built to survive volatility rather than being blindsided by it. It replaces the anxiety of market fluctuations with the quiet certainty of a well-tested "Plan B."

What is the difference between a retirement calculator and professional modelling?

Online calculators are static, "one-size-fits-all" tools that often use dangerous, linear assumptions. Professional modelling is a bespoke, research-driven process that accounts for complex Australian tax laws and the latest Division 296 thresholds. It provides a longitudinal view of your financial life, integrating your specific goals and risk tolerance. A calculator gives you a number; professional modelling gives you a disciplined strategy for the next thirty years.

Does the model take into account my partner’s superannuation and assets?

Yes, a robust model must take a holistic view of all household wealth. It integrates your partner’s Superannuation, private share portfolios, and any joint property holdings to manage the A$2.1 million Transfer Balance Cap effectively. This collective approach is essential for tax-minimisation and estate planning. It ensures that both of you have a shared understanding of your financial trajectory and the stability of your combined income stream.

Can modelling show me if I can afford to downsize my home in Sydney?

Modelling provides a precise simulation of the capital released from a Sydney property sale and its impact on your longevity. We can factor in "Downsizer Contributions" of up to A$300,000 per individual to bolster your Superannuation without it counting toward standard contribution caps. This allows you to see exactly how moving house affects your "retirement pay cheque" and your ability to fund future aged care or travel goals.

What happens to the model if I live longer than expected?

We mitigate longevity risk by running our projections until age 100 as a standard practice. While the average Australian life expectancy is lower, planning for the "long tail" ensures you don't outlive your capital. The model accounts for rising healthcare costs and potential aged care requirements in your final decade. This conservative approach provides the emotional reassurance that your lifestyle remains protected, regardless of how many years of retirement you enjoy.